As an accountant or advisor you’ve likely been considering whether to offer – or expand your offering – in sustainability reporting for your clients. For some this will have come directly out requests from existing customers – while others will be interested in diversifying their services, looking for a commercial point of difference, or simply be responding to this important business trend.

In this report we look in to the trend for sustainability reporting, and explore the pros and cons of offering sustainability reporting in an accounting practice.

In This Guide To Sustainability Reporting For Accountants:

What is sustainability reporting?

Sustainability reporting is a step beyond traditional reporting of financial results. Sustainability reporting considers the impact of the business with broader criteria, focused on its environmental, social and governance goals, or ESG. Sustainability reporting means the company must assess its environmental impact, the communities in which it operates, and its governance, auditing and reporting of those responsibilities.

In recent years it has grown in importance as consumers demand better green credentials from the businesses they patronise, amid growing concern about climate change. Companies are now turning to sustainability reporting to not only ensure they behave environmentally responsibly but also because it has become an important marketing tool.

Sustainability reporting considers the impact of a business according to broader criteria.

Sustainability reporting considers the impact of a business according to broader criteria.Who reports on sustainability?

Around the world there are requirements for certain companies to report on sustainability. For example in New Zealand, it is mandatory for companies including listed issuers, major banks, insurers, and investment scheme managers to report on climate-related risks and opportunities. This is mandated in the Financial Sector (Climate-related Disclosure and Other Matters) Amendment Act, 2021. The Act requires around 200 of the country’s major financial players to disclose information on the impact of climate change on their business, both positive and negative. Disclosures will be required each financial year from 2023. The Act is one of many changes being made by New Zealand’s government and crown entities to support sustainability reporting.

In Europe, there is also a shift toward sustainability reporting. The Non-Financial Reporting Directive (NFRD) requires companies with more than 500 staff and a high public interest, such as banks, publicly traded companies and insurers, to report on issues including pollution, human rights, diversity and social responsibility. The NFRD is being extended by the introduction of the Corporate Sustainability Reporting Directive which is aimed at increasing the quality and transparency of information being reported. Companies will need to meet obligations under the CSRD by 2024.

In the United States, the shift toward sustainable reporting is somewhat slower. However, in March this year the climate disclosure rule proposal from the SEC proposed improvements to how companies report climate-related issues. The proposal is expected to be challenged in the courts.

Why might a client request sustainability reporting?

The shift toward sustainability reporting is increasing across the world, and it is becoming a ‘must-have’, rather than ‘nice-to-have’ part of a company’s processes. Mandatory reporting regulations are now in place in dozens of countries globally, and consumers are demanding to see the green credentials of the companies they purchase from.

According to this article from Deloitte, companies need to show “greater commitment to sustainable value creation.” Those which do, the report notes, will ultimately be more viable and valuable to their stakeholders.

However businesses looking to incorporate sustainability reporting will have a number of factors to weigh up before they start the process. There are challenges to sustainability reporting and implementing new processes may depend on timing and other factors unique to the business.

Some clients may be mandated to report their sustainability performance – others will request it of their own volition.

Some clients may be mandated to report their sustainability performance – others will request it of their own volition.The pros and cons of sustainability reporting for your business clients

It’s likely many of your clients will be looking to implement sustainability reporting into their business. However there are pros and cons they will need to consider before doing so. These include:

The pros of sustainability reporting for a business

- It creates trust. Sustainability reporting shows stakeholders that the company is invested in a better environment and future for the next generations. Climate change is accelerating and a business that recognises this and implements systems that make it responsible for its impact on the environment creates trust with its employees, and its customers. It also identifies the risks and opportunities that the business will face in the near and long-term future. The increased transparency and accountability around these concerns will create a higher level of trust among all stakeholders.

- It can streamline systems. Implementing new, non-financial reporting systems inevitably creates a need to assess current systems and what is / is not working. The decision to implement sustainability reporting will require analysis of current systems and finding where workflows and processes can be improved, or better structured to meet the new requirements. This could well uncover issues within the business, such as excessive emissions or use of non-recyclables, that can be resolved or better organised to ensure the company meets the new requirements.

- It creates value for employees. There is value for all stakeholders in the implementation of sustainability reporting - including, importantly, for staff. Employee discontent and turnover is a major concern for any business, particularly in the post-covid environment and amid the so-called ‘Great Resignation.’ Implementing sustainability reporting, with the transparency and commitment required, is one way to show employees they are valued, and that the company has a long-term commitment to protecting future generations and the environment.

- It creates value for customers. Consumers are increasingly looking at the green credentials of the businesses they support. Sustainability reporting is one way to attract consumers looking for more environmentally friendly purchasing options.

- Reduces compliance costs. Adoption of data collection processes to understand a company’s non-financial outputs is likely to deliver compliance cost savings. As sustainability reporting is increasingly mandated, there will be costs associated with breaches. If a business is already set up to meet the mandated requirements it will avoid costs associated with non-compliance.

Some clients may see reduced costs, included reduced energy costs, from pursuing sustainability targets.

Some clients may see reduced costs, included reduced energy costs, from pursuing sustainability targets.The downsides of sustainability reporting for a business

- Training will likely be required. Implementing new systems will require upskilling for staff to understand how to gather, analyse and report on new data. They may require the business to frontload an investment to ensure the data collection and reporting systems are properly in place.

- It may be difficult to collect the right data and conduct audits. Understanding the data required is key to implementing sustainability reporting. The data may include analysing the supply chain, understanding the life-cycle of the products produced, assessing the emissions of the business and so on. Understanding how the data is analysed and collected may be a difficult and time-consuming process. Auditing the data and subsequent reports – which is recommended, although not always necessary – may also be a learning process.

- It requires change management. As with any shift in business strategy, the implementation of sustainability reporting will require change management among executives and staff. Change management can be a difficult process as it requires people to adjust their habits and thinking. It may be useful to bring in some support for change management if this shift will cause pushback within the business.

- Buy-in may be slow or limited. Once the decision is made to shift to sustainability reporting, the flow-on to staff needs to be clear and understood to ensure the implementation is as smooth as it can be. Even with the right support in place, employees can be slow or reluctant to change their working habits and responsibilities. It will be important to pre-empt or be ready for pushback from staff who may feel they are being asked to take on extra responsibilities, or who are being asked to upskill, or who seek pay rises on the back of the shift.

The pros and cons of sustainability reporting for an accounting practice

Sustainability reporting can be complex and time-consuming – so is it the right field for you firm?

The upsides of sustainability reporting for your practice

- Adds billable hours. Provided that your clients sees value in sustainability reporting and is willing to pay for it, bringing expertise in the field gives you a significant opportunity to engage longer and more deeply with your clients.

- Extends the total lifetime value of your customers. This is a similar point to the one above, but with a different spin: providing ESG services to your clients is a way of answering the question of ‘what next?’ Once you’ve settled into a rhythm of business guidance – and perhaps helped your client move on to some necessary business software tools such as cloud accounting or inventory management – you may well be looking for a further dimension to the guidance you offer. Sustainability reporting – for some of your clients – can be that opportunity.

- Creates recognition for your firm. Businesses around the world are shifting to sustainability reporting. Being part of this movement means being recognised globally as an organisation that understands its responsibilities to the wellbeing of its people and the future of our planet. It is a mark of responsibility that will be recognised wherever the company conducts its business. This is likely to lead to greater sales with clients looking for green credentials, along with an improved reputation and greater brand awareness.

- Future-proofs your customers. A business that implements sustainability reporting is in many ways future-proofing itself, along with protecting the planet. The process of understanding the data required, finding ways to improve and innovate, partnering with likeminded companies and creating trust within the business all go some way to ensuring the business is well placed for future growth. Perhaps most importantly, however, a business which implements sustainability reporting is adopting a standard that is increasingly sought out by consumers who want to spend their money with an environmentally responsible organisation.

- Identifies opportunities. Implementing sustainability reporting opens up new opportunities and can initiate innovation within your own practice. By introducing the concepts of non-financial benefits, business leaders, partners and staff alike will likely identify ways in which your business can operate better to support its environmental objectives. This may be identifying ways in which emissions can be reduced, ways in which waste can be reused, or initiatives such as wellbeing days within the organisation.

Helping your clients report their ESG performance can deepen your engagement with them, and increase your billable hours.

Helping your clients report their ESG performance can deepen your engagement with them, and increase your billable hours.The downsides of sustainability reporting for your practice

- Reporting requirements are inconsistent and can be unclear. Sustainability reporting requirements are inconsistent around the world, with governments moving at different speeds and requiring different outputs. And while some elements are mandatory in some countries, they are also open to interpretation, which can lead to confusion around data, reporting and any possible breaches. Becoming an expert in this space represents a major challenge.

- Upfront investment required. Getting started in this space will inevitably require upfront investment which may place a strain on the business. Training and programme design will take time, and cost money that you won’t immediately recoup – especially if you hire someone in to start the team.

- Data collection is complex. Data collection is a key part of sustainability reporting. However, collecting certain data sets - such as an understanding of ethics and human rights associated with suppliers, or the output of emissions throughout a product’s lifecycle - can be very difficult for your clients. Working with incomplete or inadequate data can be a frustrating experience for you and your team and has the potential to undermine your whole project.

- New staff may be required. Sustainability reporting requires certain skills around analysis and collection of data, and a clear understanding of that information is needed to meet stakeholder expectations and / or mandatory requirements. Your firm may not have the skills in place to meet these requirements, and may need to hire new staff to help build your ESG reporting team. As such a risk / reward assessment should be carried out before any decisions are made.

- Doubt around impact. Beyond the difficulties of implementing sustainability reporting, there are doubts about its impact. As this article points out, during the last twenty years of increased sustainability reporting, “carbon emissions have continued to rise, and environmental damage has accelerated. Social inequity, too, is increasing.” In short, not all ESG reporting formats – or indeed customers – will make any progress with sustainability reporting, and the reputational risks involved should be weighed before you begin an engagement with a client or a particular programme.

Sustainability reporting for SMEs

While mandatory sustainability reporting is generally required only for large or public interest companies, SMEs may want to move to sustainability reporting to gain from the benefits.

However, SMEs can face greater challenges when considering the adoption of sustainability reporting, due to their smaller size. If they have a budget, they can seek support from external experts in the sector or consider guidance from papers such as these, which outlines a set of decision criteria, allowing for a methodological ‘best-worst case’ of moving toward this form of reporting.

Without support, shifting to further reporting may well prove arduous. As this Europe-focused paper points out, “the overwhelming majority of SMEs perceive sustainability reporting as a burden, and it appears that SMEs either do not have the capacity to comply or are reluctant to invest the necessary resources.” There are, however, a number of standards and guides in place which an SME will find useful when looking to implement non-financial reporting.

There are many different sustainability reporting standards, and it's important to choose a credible framework.

There are many different sustainability reporting standards, and it's important to choose a credible framework.What are the different sustainability reporting standards?

Integrated reporting

The IFRS Foundation is a not-for-profit organisation created to develop globally accepted sustainability disclosure standards. It has developed the standards for integrated reporting, which requires a business to have a cohesive approach to its outputs and clearly outline all risks and opportunities that will affect its value creation over time.

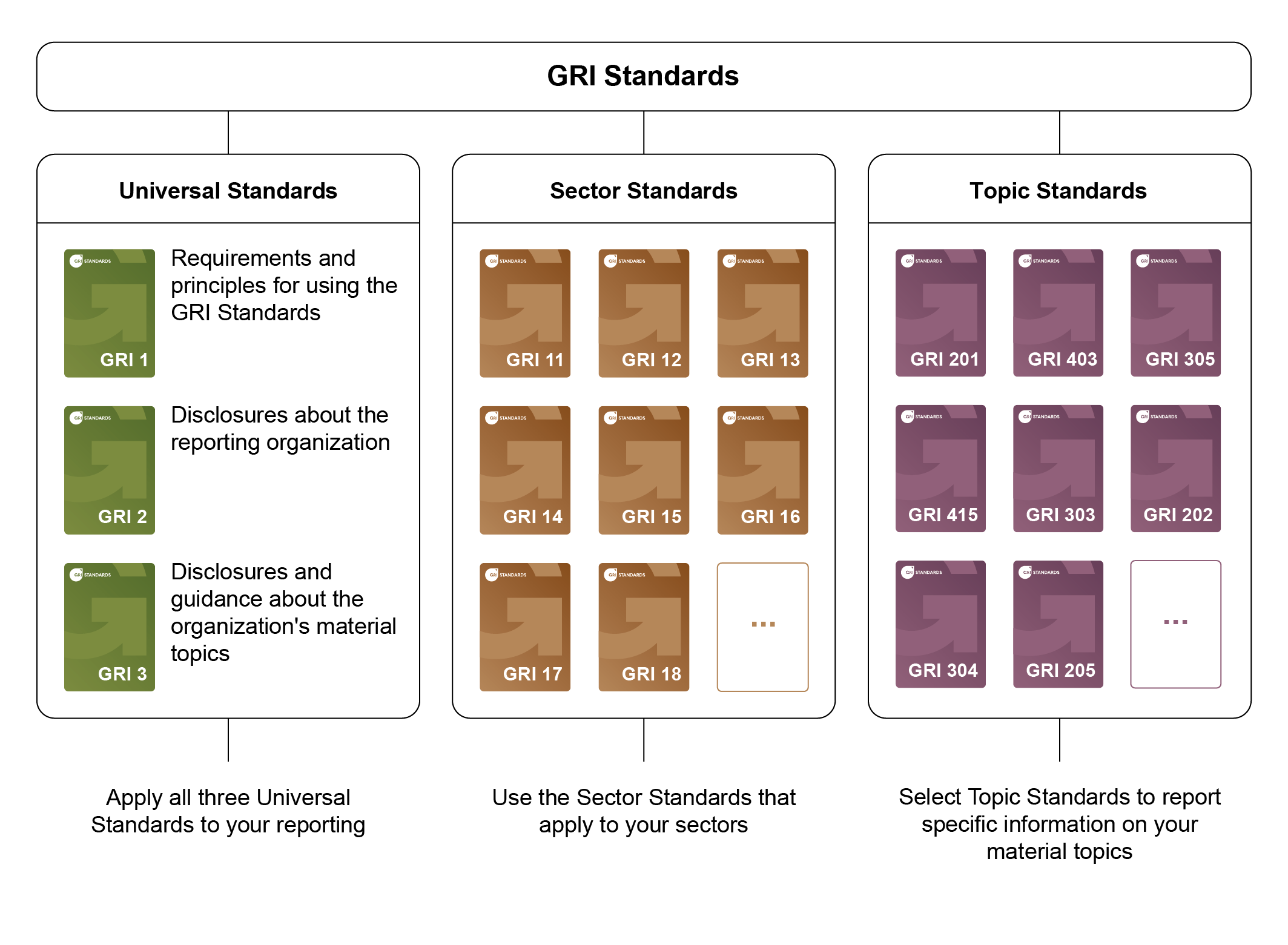

GRI sustainability reporting

The GRI Standards are designed to enable businesses of any size to understand their impact on the environment and people in a globally recognised way. The standards are outlined in a modular ‘set’ of requirements for a business to implement. There are also sector-specific and universal standards which may be relevant depending on the business and its aims.

{kind=link}

TCFD reporting

The TCFD was set up by the Financial Stability Board to advance the reporting of climate-related financial information. The TCFD makes recommendations on the information that should be disclosed by companies to support stakeholders including investors and lenders to be able to price and assess various risks associated with climate change.

Other global sustainability reporting standards

Beyond the commonly used standards outlined above, there are other reporting standards and guides available to organisations looking to implement non-financial reporting.

For example, there is the UN Global Compact, which is voluntary and set up for companies willing to change their business operations and incorporate the Compact’s Ten Principles. There is also the PRI, or Principles for Responsible Investment, which outlines six principles for an organisation to consider should it want to incorporate ESG issues into its investment practice. It has signatories around the globe and calls itself the “world’s leading proponent of responsible investment.”

Where is sustainability reporting mandated?

Around 25 countries around the world have introduced some form of mandate for certain companies to disclose ESG information. This includes the United Kingdom, South Africa, Australia and New Zealand. It is important to note reporting requirements and standards are being reviewed and advanced at some speed both internationally and at country levels. Any business wanting to implement this type of reporting will need to research the latest information within its operating jurisdictions.

What do the Big Four have to say about sustainability reporting?

- EY recently released its ‘Enough’ report which explores the idea of corporate sustainability over the last 30 years, and how it has adapted. It takes a hard-hitting approach to sustainability now, saying there are “clear aspects that need to change.”

- KPMG is also extremely active in this space, with its CEO Outlook Pulse Survey 2021 showing a massive 89% of CEOs want to build on sustainability gains made during the pandemic.

- Another of the big four, Deloitte, also surveyed CEOs on sustainability reporting but found multiple disconnects between the motivations, the actions and the subsequent impact.

- PWC, meanwhile, has created the concept of ‘The New Equation’ which it says “reflects fundamental changes in the operating environment” including climate change.